Burtnett Insurance Agency Blog |

|

Are firearms covered under homeowners insurance?  No matter how carefully you clean and maintain your firearm, unexpected things can happen. Even if you store them in a fire-resistant safe, there is no guarantee that they won't be severely damaged in the event of a disaster.

For this reason, many people choose to purchase insurance for their firearms. There are a number of companies and organizations that provide specialty firearm insurance. However, before you purchase a separate policy, make sure to check with your homeowners or home insurance company and ask if they provide coverage for firearms. Most home insurance policies have a section called "unscheduled personal property" which provides some amount of coverage for personal belongings that aren't otherwise listed. This might include items such as computer equipment, but can often cover firearms as well. That having been said, keep in mind that insurance companies often have coverage limits for firearms, not just in terms of a dollar amount, but the specific quantity of firearms. In other words, they may place a limit on the number of guns the policy will replace in the event that they are destroyed in a covered disaster. As always, policy specifics vary from provider to provider, so be sure to ask yours about firearm coverage limits.

0 Comments

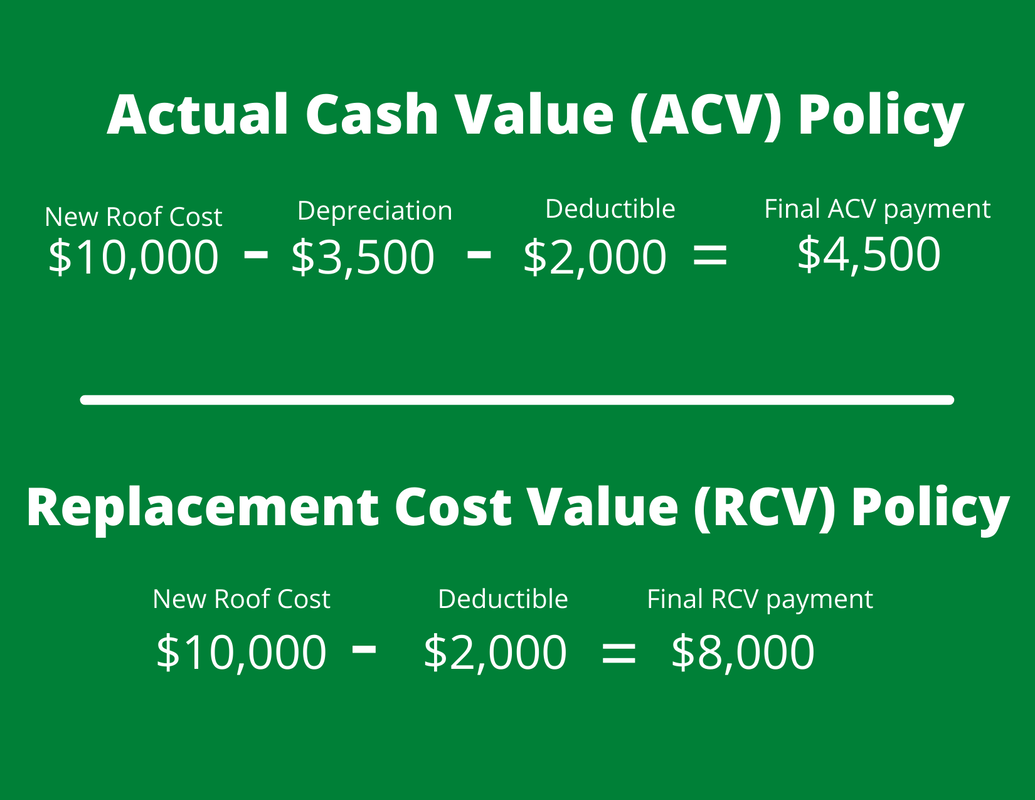

When your property is damaged or destroyed, you know that your insurance provider will write a check to help cover the loss. But do you know exactly how the value of that check is determined? Will your insurance provider pay the actual cash value or the replacement cost of the damaged property? What is the difference between the two, anyway? Understanding these concepts is essential to understanding your insurance policy, so today, we're taking a closer look at actual cash value vs. replacement cost - read on!  Is actual cash value the same as replacement cost? What's the difference? When you think of the monetary value of a particular piece of property, how do you arrive at a number? Do you think back to the sticker price you paid at the store? If it's a relatively recent purchase, that may be fairly accurate, but what if you've owned the property for a few years? Do you factor in wear, tear, and depreciation? These are all important things to consider, especially when it comes to replacing a piece of property damaged by a covered loss. That's why insurance companies generally divide the value of a reimbursement into two categories: actual cash value (ACV) or replacement cost (RCV). They may sound relatively similar, but they actually can function quite differently. Actual cash value coverage To begin, let's take a look at a plausible example. Let's say that you recently purchased a brand new TV for $4,000, and unfortunately, it was destroyed in a fire. If the personal property portion of your home insurance uses ACV, the payment will likely be less than the initial $4,000 you paid at the store. This is because ACV takes the initial cost of the item and deducts depreciation from it. So, how does a claims adjuster determine depreciation? In many cases, they don't (or can't) inspect the piece of property in question directly. Instead, the value is based on the "life span" of the item. If your TV had a life span of 10 years, then it would have $400 per year deducted from the ACV for every year that you owned it. In this case, if you had this TV for three years before the fire, it would have depreciated by $1200, and the ACV payment from your insurance company would be $2800 (minus your deductible, of course). This is just an example, and the method by which a carrier determines an item's value and life span will vary from company to company. Regardless of the particular method used, the life span value is meant to account for the normal wear and tear property undergoes, as well as the normal decrease in value that most items experience over time. For example, a TV isn't likely to increase in value, or even maintain its value over the years. Even if it's in great condition, the older it becomes, the more its value has depreciated. Replacement cost coverage Replacement cost coverage is a little more straightforward. This refers to a payment which equals the initial cost, or the cost you would have to pay to replace the property today, without factoring in depreciation.  Let's look at the example of our unfortunate TV that was lost in a fire. If your insurance policy coverage is RCV, it would pay to replace your property at full cost (again, minus your deductible). In other words, it would allow you to buy a new TV, or one that was similar in kind and quality to the one you lost in the fire. Of course, this payment won't exceed the personal property coverage limits outlined in your policy. That's why it's important to make sure that your coverage limits are equal to the value of the property you're insuring. Whether your coverage is ACV or RCV, if you have high-end electronics, expensive art, or other rare and expensive valuables, you may need to consider an additional endorsement to your existing policy. Depending on your coverage limits, the personal property portion of your homeowners insurance policy may not be enough to cover RCV reimbursement for such items. How do I know whether my insurance policy uses actual cash value or replacement cost reimbursement? If you already have an insurance policy, such as a home or property policy, then you'll want to review your declarations page. This document simply outlines the specifics of your policy. In addition to stating whether your coverage is ACV or RCV, it should show other helpful information, such as your premium, your coverage limits, and any deductibles you may have. If you need another copy of your declarations page, your insurance provider or agent should be able to help you get a hold of one. How does actual cash value and replacement cost coverage work with different insurance policies? Homeowners insurance. Coverage is normally split between personal property coverage and dwelling coverage. Most homeowners insurance offers replacement cost coverage for the dwelling (your actual home), and possibly other structures, such as a storage shed or detached garage. On the other hand, the personal property portion of your coverage will more than likely be actual cash value. However, many insurance carriers will allow you to upgrade your personal property coverage from ACV to RCV if you are willing to pay a higher premium. It is important to keep in mind that the type of coverage offered will likely depend on the age and condition of your home. This is especially true for your home's roof - while your dwelling may be covered at RCV, if your roof is old or worn, it may only be covered at ACV. Renters insurance. As you may know, renters insurance is designed to cover your personal belongings inside a home that you rent rather than covering the dwelling itself. Like homeowners insurance, the type of coverage your renters insurance offers will depend on your carrier and the specifics of your policy. While renters insurance coverage is often ACV, it is certainly possible that your provider offers an upgrade to RCV. Fortunately, renters insurance is often affordable, and policyholders can typically get RCV while maintaining a relatively low premium. Auto insurance. Cars are notoriously bad at maintaining their value, and it is often said that they begin depreciating the moment you drive them out of the dealership. For this reason, auto insurance coverage is normally actual cash value and many insurers do not offer replacement cost coverage. Those that do will often do so through an endorsement, although they will usually have fairly strict requirements in terms of the vehicle's age and mileage. Which is better: actual cash value or replacement cost? Generally, receiving the replacement cost as reimbursement is more helpful for policyholders than actual cash value coverage following a disaster or incident of theft. If you're concerned that your property won't be adequately covered with ACV, then RCV could be just the thing you need. However, selecting this option for your policy will come at a greater premium, sometimes substantially so. Furthermore, your carrier may have strict guidelines or restrictions regarding what property they will cover at replacement cost, and what condition it must be in before they will do so. For these reasons, it is difficult to say that one option is better than the other in the long run as it will depend on your specific insurance needs - you may find that changing your policy to RCV isn't worth the increased premium. If, for example, you live in an area that has a very low risk of disasters or theft, or if you simply don't have a lot of property to cover, you might be satisfied with the coverage that ACV provides. While RCV is recommended for certain property (like your home), you may find that other less valuable items simply don't justify the increased premium.

If you're shopping for insurance and trying to decide whether or not you should go with actual cash value or replacement cost coverage, you should always speak with your insurance provider or insurance agent for further guidance. However, at the end of the day, only you can decide what type of coverage is best for you! |

Contact Us(817) 220-7682 Archives

January 2023

Categories |

RSS Feed

RSS Feed